New wireless competitors took over half of mobile sub adds in 2024

By Ahmad Hathout

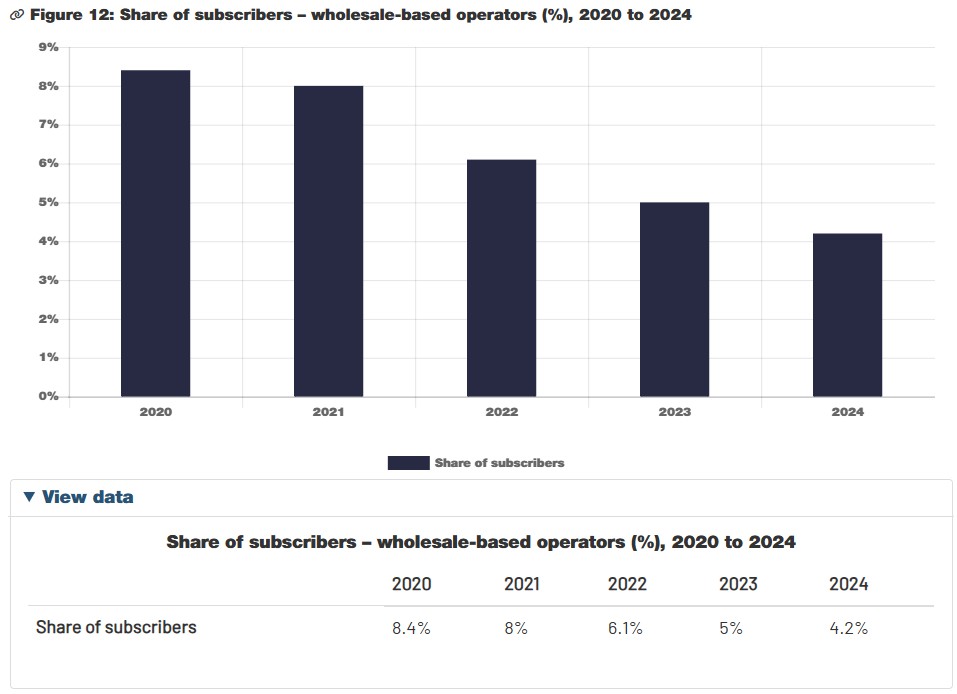

Independent wholesale-based internet service providers lost half of their market share since 2020, according to a report from the CRTC.

The market share dropped from a high of 8.4 per cent in 2020 to 4.2 per cent in 2024, according to the Canadian Telecommunications Market Report, released Tuesday. And it’s been steady in between: falling to 8 per cent in 2021, 6.1 per cent in 2022 and 5 per cent in 2023.

“With shifts in the internet service market and in response to recent policy decisions, the wholesale model is evolving and other types of wholesale-based providers are emerging,” the report said. “The CRTC continues to monitor these shifts and their impact on competition.”

Independent operators would not be so diplomatic in describing the state of the market. They have argued that, for years, the wholesale access rates have remained too high, with several independents getting absorbed by the larger players and others pleading for the regulator to address what they claim are predatory pricing strategies by the larger players that are squeezing them out.

Now, these smaller providers are wondering if the CRTC’s policy allowing the three largest telecoms to access their internet networks will exacerbate the problem. The CRTC said it will track the use of wholesale fibre services by large ISPs in future reports.

In the meantime, between 2020 and 2024, the report noted that legacy telcos took more revenue share – from 40 per cent to nearly 46 per cent – than cable-based operators, which saw a decline from 44.4 per cent to 40 per cent. The CRTC said this was due to subscribers opting for direct fibre. Other operators took one-per-cent less share over that period.

The report noted higher subscriber churn in 2024, at 1.56 per cent, compared to the 1.52 per cent in 2020, demonstrating that there was more switching.

Internet prices for some benchmark tiers also declined from January 2021 to September 2025. The price for the federal objective speeds of 50 Mbps download and 10 Mbps upload dropped from approximately $82 at the beginning of 2021 to $60 in September 2025. One gigabit download and 15 Mbps upload speeds dropped from $121 to $81 over the same period. However, 2 Gbps and 15 Mbps upload increased by $3 from November 2023, when it was $115, to September 2025.

In Ontario, prices for the 1 Gbps/15 Mbps and 1.5 Gbps/15 Mbps were also down from about $118 in January 2021 to $77 in September 2025 for the former and from $130 to $113 for the latter. The 2.5 Gbps/15 Mbps speeds were also down about $10, from April 2023, when it was $150, to $140 at September 2025.

Houses with access to gigabit-speed services increased across the board from 2020 to 2024, with all of Canada being at about 90 per cent and rural and First Nations reserves being at 55.2 per cent and 44.3 per cent, respectively.

The percentage of households covered by a fibre network increased about 20 per cent in Canada to 72 per cent in 2024, while it increased by approximately the same percentage in rural areas to 45.2 per cent.

A total of 31.5 per cent of subscribers were on gigabit or higher speeds in 2024, up from 8.3 per cent in 2020; 70.5 per cent were on 100 Mbps and higher; and 85.5 per cent were on 50 Mbps and higher.

By September 2025, median download and upload speeds were 250.4 Mbps and 85.2 Mbps, respectively; for rural Canada, the media speeds were 129.3 Mbps and 32.1 Mbps.

The share of those on fixed wireless and satellite was up to 7.5 per cent in 2024 compared to 6.5 per cent in 2020.

The average monthly data usage in 2024 was 585.5 gigabytes, up from 385.6 in 2020. The monthly average revenue per user (ARPU), however, was up from $63 in 2020 to approximately $67 in 2024.

Internet prices declined or remained steady as inflation increased from the January 2021 period.

By the spring of 2025, Canadians were feeling more confident in their ability to pay for internet service and fewer were reporting that it was becoming less affordable over the year, the report said. At 45 per cent, fewer Canadians were finding internet service becoming less affordable since the CRTC launched its biannual public opinion research tracker in the fall of 2023, when that percentage was 51 per cent. A lower rate of low-income households were also reporting that it was becoming less affordable, from 49 per cent to 42.6 per cent.

To aid in affordability, the CRTC found that Canadians changed their home internet plans at a higher rate, from 6.7 per cent in the fall of 2023 to 15 per cent in the spring of 2025. The rate of switching for low-income households was nearly double over that period, to 18.6 per cent.

New competitors take their share of mobile wireless subs

The report also found that new competitors – those not named Rogers, Bell and Telus –took over 55 per cent of mobile wireless subscribers added in 2024, which it said was evident in Ontario, Quebec, the Maritimes and western Canada.

The trend has emerged as Quebecor’s Freedom Mobile branches out and mobile virtual network operator (MVNO) deals are struck with the larger players.

“Given take-up of the MVNO service in 2024 and MVNO operators gaining subscribers in large markets, national market concentration could decline in 2025,” the report said.

Rogers, Bell and Telus (Big Three) and their flanker brands saw their market share decline slightly, from 86.5 per cent in 2020 to 85.9 per cent in 2024, while others have increased share from 13.5 per cent to 14.1 per cent over that period.

Prices for mobile plans – specifically 10 GB, 50 GB and 100 GB – have declined from 2021 to September 2025. A 10 GB plan in January 2021 would have cost you about $71; by September 2025, it would set you back $41. A 50 GB plan went from $123 to $53. And a 100 GB plan went from $170 to $66.

Adoption of data plans of 50 GB or more skyrocketed from 5.2 per cent in 2020 to 56 per cent in 2024, and from 42 per cent to 85.3 per cent for 10 GB or more. Average monthly data usage also jumped from 3.7 GB in 2020 to 8.8 GB in 2024.

For the Big Three, revenue per GB of data was down from $9.5 to $4.5 from 2020 to 2024, while other providers went from $4.1 to $4.42 over that period of time.

Like internet services, mobile wireless prices have declined and remained stable in the face of rising inflation, with fewer people reporting cellular services becoming less affordable over the year.

“Nearly half of Canadians now agree that they have enough choice in cellphone service providers, a slight increase since Fall 2024,” the report said. “This perception has also improved in rural areas, though residents there remain mostly neutral. Agreement is highest among Francophones, seniors, Canadian newcomers, Quebec respondents, and urban residents.”

In the fall of 2023, 8.5 per cent of people reporting that they made changes to their mobile services due to affordability, which increased to 21 per cent in the spring of 2025. For low-income households, that percentage was up from around 11 per cent in 2023 to 26 per cent in 2025.

Subscriber churn was up, from 1.14 to 1.22 per cent over that period.

“Public perception of affordability in mobile services generally improved, with Canadians showing greater confidence in their ability to pay for such services, or else switch to more affordable (or otherwise preferable) options,” the report said. “This is significant, since Canadians have become more avid users of data, and the share of mobile subscribers with 50 GB or more of data has tripled since 2022.”

5G networks reached nearly 95 per cent of the country in 2024, up from 53 per cent four years earlier. In rural Canada, it jumped from about 16 per cent to 75 per cent over that period, and from about 20 per cent to 52 per cent in First Nation reserves.

The report also noted that Canadians found their mobile networks to be more reliable in 2025 than in previous years, particularly in rural Canada.